大家好!“美国退休账户详解” (All About Retirement Accounts)这套课程终于上线啦!被大家呼吁了2年多,我终于克服了拖延症把这套课程做出来啦!

购买链接如下:

别忘了用 coupon code “MONEY322”,获取50%的折扣!

这套课程分40个小节,涉及了美国常见退休账户的方方面面。有基础知识,比如401K和IRA的区别,Backdoor IRA如何操作;也有实操中常见的细节问题,例如Roth IRA存多了怎么办?留学生要回国了401K怎么办?Backdoor操作的时候被扣税了怎么办?

内容以我频道里的原视频为骨架,补充了视频没有的知识点,整合加工完成。我在整套课程里有意地把知识点串联梳理起来,由浅入深、系统地呈现给大家。作比较、列数据、讲实操、作总结,同一个知识点在不同场合反复出现,我就从不同的角度反复地说它。保证你在看完这套课程之后能把之前一些似懂非懂模模糊糊的概念全部吃的透透的。(第315期“Mega Backdoor”就是课程的节选,想要了解课程风格的朋友欢迎试听第315期)

每一个必要的场合都配了例子,每个例子都配了数字。该有的图表,分析等等都给它配起来。涉及计算的时候拿数字说话,还融合了原频留言区的观众留言(有观众提的好问题也有有价值的补充)。

我对这套课程的内容非常有信心,希望能够帮到有需要的朋友!

购买链接如下:

别忘了用 coupon code “MONEY322”,获取50%的折扣!

大纲如下:

前言

1. 401K

1.1 什么是401K

1.2. How does 401K plans Work

1.3. Contributing to a 401K

1.4. How does a 401K make money

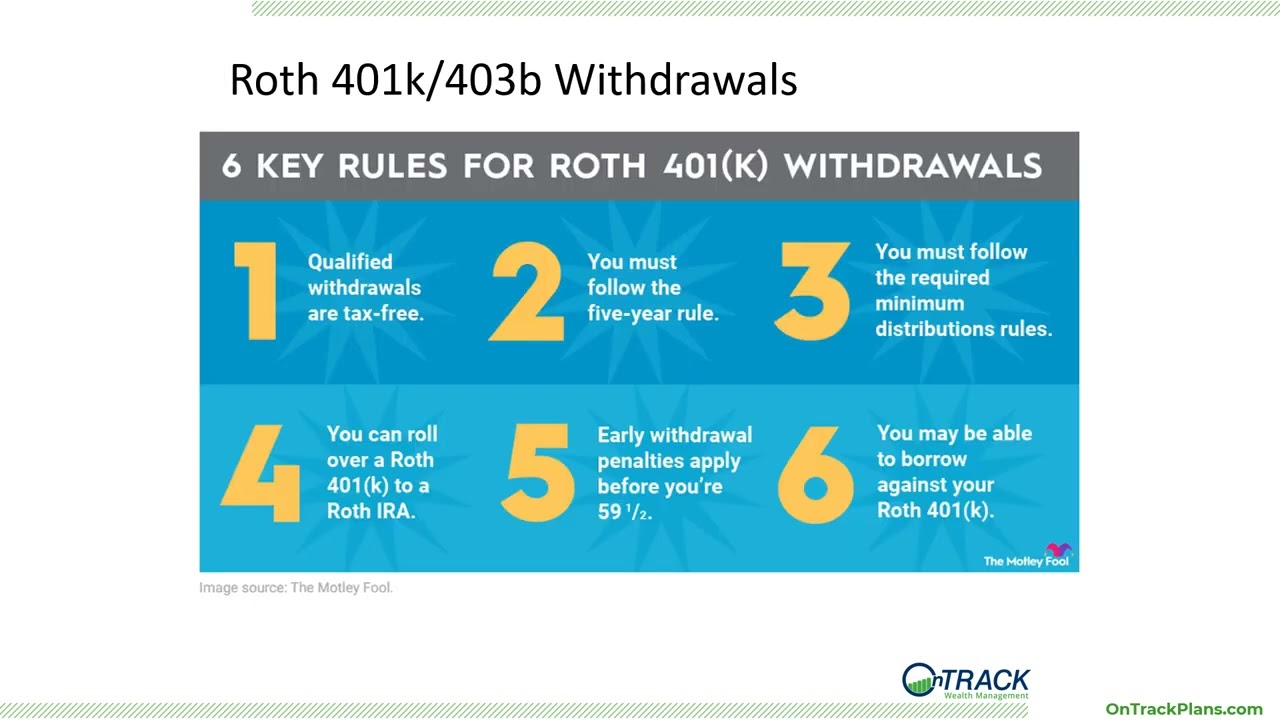

1.5. Withdrawals from 401K

1.6. 离职之后401K 的match问题

1.7. 离职之后401K怎么处理

1.8 Roth 401K里面雇主match的钱是税前的还是税后的

1.9. 401K Loan

1.10. Traditional 401K Vs. Roth 401K

2. 回国之后退休账户怎么办?

3. IRA

3.1. IRA 简介

3.2. 什么是Earned income

3.3. IRA 有什么优点

3.4. IRA有什么缺点和限制

3.5. 未来的税率问题

3.6. Roth IRA简介

3.7. 什么是税前的钱?什么是税后的钱?

4. Roth IRA

4.1. Roth IRA简介和Roth IRA与传统IRA相同的地方

4.2. Roth IRA 和IRA不同的地方

4.3. 从Roth IRA中取款的问题

4.4. Roth IRA 不qualified怎么办

4.5. 什么是recharacterization

5. Backdoor IRA

5.1. Backdoor IRA

5.2. 传统IRA里面既有税前的钱又有税后的钱

5.3. 传统IRA mixed,避税方法

5.4. backdoor IRA 8606

5.5. 股票跌了?为什么不抓住这个机会做Backdoor IRA?

5.6. Backdoor IRA不要用roll over的钱交税

5.7. Mega Backdoor Roth Strategy

6. 美国税法中的“收入”

6.1. 美国税法中的“收入” – 简介

6.2. 美国税法中的“收入” – Gross Income

6.3. 美国税法中的“收入” – AGI

6.4. 美国税法中的“收入” – Taxable Income

6.5. 美国税法上常见的几种收入- MAGI

6.6. 401K Deduction

7. Self-Directed IRA

8. 孩子的退休账户

8.1. 给孩子开Roth IRA

8.2. 529计划可以转成Roth IRA

9. 结束语

***************************************************************************************

大家好!欢迎通过如下链接加入会员“谈钱也谈情”(Money & Life):会员福利包括会员专属视频、频道更新等等。谢谢大家的支持和鼓励!

如果您想“和我一起来谈钱”,欢迎写电邮到 AskWei@chattymoney.com 来信请在标题注明“访谈”。正文内容请大致介绍您在哪方面有心得体会/经验教训/投资机会/理财历程,或其它一切跟钱有关系的有趣有料的话题。

如果您想帮我把频道做的更好,欢迎点击如下链接打赏/One time Donation – Thank you!

…(read more)

LEARN MORE ABOUT: IRA Accounts

TRANSFER IRA TO GOLD: Gold IRA Account

TRANSFER IRA TO SILVER: Silver IRA Account

REVEALED: Best Gold Backed IRA

How to Choose Between Roth 401(k) and Traditional 401(k)? How to Choose Between Roth 401(k) and Roth IRA? (Issue 322)

retirement planning can be a daunting task. Among the many decisions to make, one of the most important is choosing the right retirement savings account. In the United States, two popular options are the Roth 401(k) and the traditional 401(k). Additionally, many individuals ponder over whether to opt for a Roth 401(k) or a Roth IRA. Let’s dive into the details and explore the factors to consider when making these decisions.

Firstly, let’s differentiate between a Roth 401(k) and a traditional 401(k). Both are retirement savings plans provided by employers, but they differ mainly in terms of tax treatment. In a traditional 401(k), contributions are made with pre-tax dollars, reducing your taxable income in the present. However, withdrawals during retirement are taxed at your ordinary income tax rate. On the other hand, with a Roth 401(k), contributions are made with after-tax dollars, meaning they are included in your taxable income. The advantage comes later – qualified withdrawals in retirement are tax-free.

So, how does one choose between the two? The decision largely depends on your current and future tax situation. If you expect to be in a higher tax bracket during retirement, a Roth 401(k) might be more advantageous. By paying taxes on your contributions now, you avoid paying potentially higher tax rates in the future. This is particularly beneficial for individuals early in their careers or those who have many years remaining until retirement. However, if you anticipate being in a lower tax bracket during retirement, a traditional 401(k) may be the better choice. It allows you to reduce taxable income now and pay taxes later, potentially at a lower rate.

While some employers provide both Roth and traditional 401(k) options, others offer only one. If your employer offers both, you may want to consider diversifying your retirement savings. It allows you to hedge your bets by having both tax-free and tax-deferred income streams in retirement. This strategy can provide flexibility when it comes to managing your tax liabilities during retirement, as you can choose which account to withdraw from based on your tax situation at that time.

Now, let’s address the dilemma of choosing between a Roth 401(k) and a Roth IRA. A Roth IRA is an individual retirement account that is not employer-sponsored, unlike a Roth 401(k). One key difference is the contribution limit – for 2022, the maximum contribution limit for a Roth 401(k) is $20,500 (plus an additional $6,500 for individuals aged 50 and above), whereas a Roth IRA has a lower contribution limit of $6,000 (plus an additional $1,000 catch-up contribution for individuals aged 50 and above).

The decision between a Roth 401(k) and a Roth IRA depends on the access you have to these accounts. If your employer provides a Roth 401(k) option, it may make sense to utilize it as it allows for higher overall contributions. Additionally, a Roth 401(k) has no income limits for eligibility, while a Roth IRA does. Therefore, if your income exceeds the limit set by the IRS, you are ineligible for a Roth IRA. However, if your employer does not offer a Roth 401(k), or if you have already maximized your contributions to a traditional 401(k), a Roth IRA can be an attractive alternative.

In conclusion, the decision between a Roth 401(k) and a traditional 401(k) hinges on your current and expected future tax situation. If you anticipate being in a higher tax bracket during retirement, a Roth 401(k) may be more suitable, whereas a traditional 401(k) makes sense if you expect to be in a lower tax bracket. If possible, diversifying your retirement savings between both options can offer flexibility. When evaluating a Roth 401(k) versus a Roth IRA, consider contribution limits and employer availability. With careful consideration of these factors, you can make an informed decision that aligns with your financial goals and retirement needs.

大学faculty的情况还真是挺不一样的,尤其是403b的roth选择

是不是可以简单理解为,假设税率不变,如果你认为你现在收入比退休后取401k时多,那就存普通401k,反之就存Roth 401k

笑死 孩子还想继承我的roth 401k 不给他点debt就蛮好了 还惦记我的钱

很多人离职或退休时(90%)都会继续将401K留在原公司,換成年金。建议大家Roll Over到外面IRA戶头,以联邦最大退休计划“ TSP “为例,所能选择投资有限:现金市场,固定CD, 国债,指数基金,外国市场;而且一个月限制交易两次,外面IRA可方便了,ETF,个别股票,期权当然还有公债,公司债,地方债……!

我是先填满401K,再放mega Roth 401K

不朝阳的面部需要补光。

钱姐你好,能讲一下after tax 401K吗?当我的pre tax 401K额度用满了,就不能给Roth 401K供款了。不过还可以供款到after tax 401K然后当天转到Roth401k。能不能谈一下这方面的利弊和选择?

強烈建议,剛出校门的年輕人如有資格參加Roth 410K一定不要錯過,不要小看一年上限$6500,五十㱑后再多一千,40年后退休将有$3百万(10%年回報)放入总額約$27万,这$273万获利一次性領出完全免稅!

你好 钱姐spacex怎么投呢 能否介绍下 谢谢

感谢钱借更新!请问可否更新一期讲讲 “after tax Roth in plan conversation” 谢谢钱姐!