So you know how much you want to contribute to retirement. But how do you split it between different retirement vehicles to get there? Today I’m sharing how we make these calculations to determine our annual retirement contribution amount.

Budget Template:

Budget Breakdown Course:

Budgeting For Baby course:

Budgeting For Baby workbook: …(read more)

LEARN MORE ABOUT: IRA Accounts

TRANSFER IRA TO GOLD: Gold IRA Account

TRANSFER IRA TO SILVER: Silver IRA Account

REVEALED: Best Gold Backed IRA

When it comes to retirement planning, one of the most important decisions you can make is how to allocate your contributions between a 401K and a Roth IRA. Both of these retirement accounts offer tax advantages and can help you reach your retirement goals. However, it is important to understand the differences between them in order to make the best decision for your individual situation.

A 401K is a retirement savings plan offered by employers. It allows you to make pre-tax contributions to an account that grows tax-deferred. This means that you do not pay taxes on the contributions or the earnings until you withdraw the money in retirement. Employers may also offer matching contributions, which is essentially free money.

A Roth IRA is an individual retirement account that allows you to make after-tax contributions. This means that you pay taxes on the contributions now, but the earnings will grow tax-free. Additionally, you can withdraw the contributions at any time without penalty.

When it comes to deciding how much to contribute to each account, there are a few things to consider. First, if your employer offers matching contributions for your 401K, you should contribute enough to take advantage of the full match. This is essentially free money, so it’s worth taking advantage of.

If you have additional money to contribute, you should consider your individual tax situation. If you think your tax rate will be higher in retirement, then you may want to contribute more to a Roth IRA, since you’ll pay taxes on the contributions at your current rate. On the other hand, if you think your tax rate will be lower in retirement, then you may want to contribute more to a 401K, since you’ll pay taxes on the earnings at your lower rate.

Finally, you should also consider your risk tolerance and time horizon. A Roth IRA may be more suitable for younger investors who have a longer time horizon and are willing to take on more risk. On the other hand, a 401K may be more suitable for older investors who have a shorter time horizon and are looking for more stability.

Ultimately, the decision of how much to contribute to a 401K and a Roth IRA is a personal one. It’s important to consider your individual tax situation, risk tolerance, and time horizon in order to make the best decision for your retirement goals.

We were looking into a Roth IRA and then learned from our tax advisor that there is an AGI contribution limit on it too that limits your ability of being able to use this. Really sucked because I wanted to explore this route and learned that it is not possible

I would definitely want to see how you are saving for Peter, how did you guys decide how much to contribute to his 529, how did y’all decide a 529 was a good fit for your family, are there other ways/accounts that you are saving for him? Our son is a touch older than Peter and we have completed baby step three.

Enjoyed the explanation and strategy, the only other thought is that if the contributions to the 401k are pre-taxed it takes less money from your paycheck to reach the maximum versus the Roth IRA where the contributions are post taxed and therefore there's a bigger bite out of your paycheck.

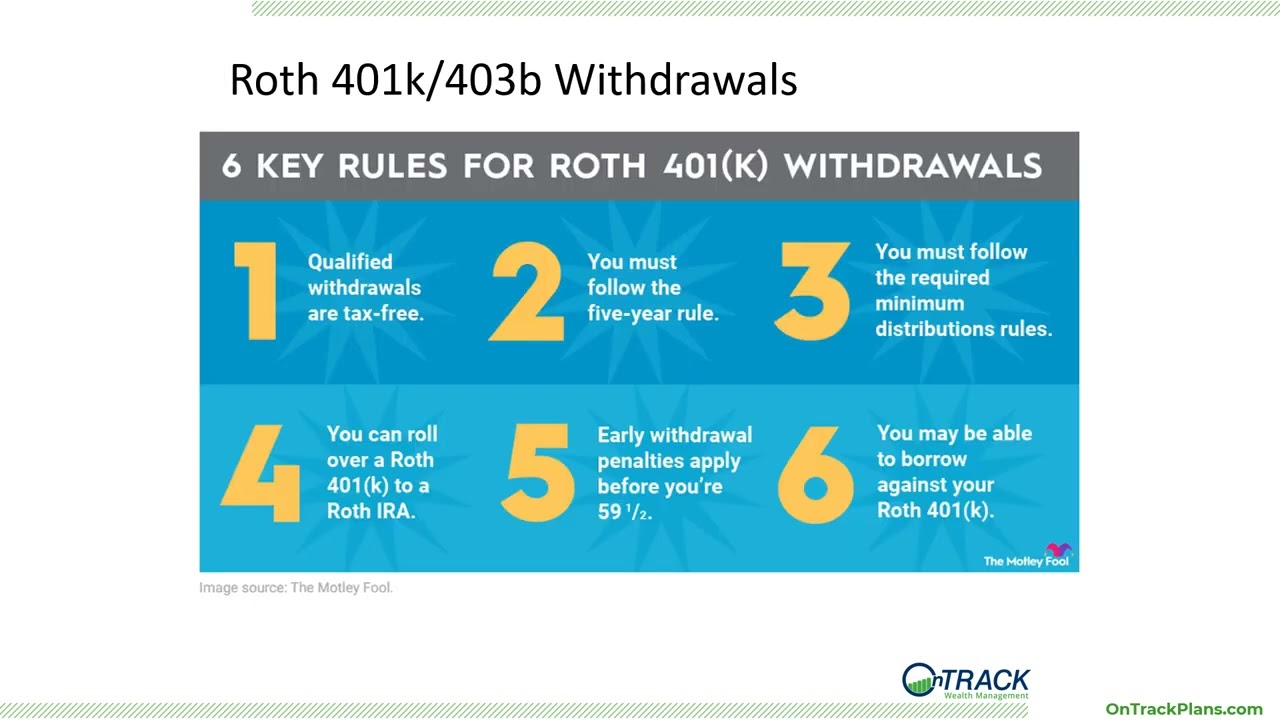

I can do a Roth 401k with my employer but correct me if I'm wrong I can withdraw contributions of a Roth IRA without penalty and you can start withdrawing earlier anyway, 59.5. Trying to figure out I want to do.

here in california the jobs only pay 20k per person , which isnt even enough for bare necessities unfortunately

Great video!! Thanks for the concrete example & showing the math/formula.

Quick question on Roth 401k – my employer has a Roth 401k option too with a 6% match I’ve been contributing to for the last 4-1/2 years. Should I open a Roth IRA too, or simply contribute more to the Roth 401k (since it has the same tax benefits) – perhaps raise it to 10%? I noticed a comment below regarding the vesting period with employers – is this perhaps a potential drawback to only using the Roth 401k?

If both spouses have gotten their employer match and fully funded their Roth IRAs, it's worth it to take a look at both 401Ks to see if there's an advantage to focus on one over the other. Are the investment options within the 401Ks different? Which one has a better vesting schedule? Which one has lower fees and better expense ratios?

A few points to touch on about 401(k) versus Roth IRA. Putting the entire 15% into their 401(k) and nothing into the Roth IRA restricts some things. Such as their company might have a vesting period and they could lose a lot of their matches if they were to get fired or quit their job before the vesting period is over. Also, not suggesting to do this but, you can always take out Roth contributions in times of need without any penalty.

We don't know how to calculate MAGI to see if we qualify for ROTH IRA This year.

Thank you. Please do a video on 529's. How do I know if I'm putting enough or too much in the 529? I noticed you put in $200/mo. How did you come up with that number?

Great video! Always get that match first then max out the Roth IRA. After that you have many options……max out HSA, max out 401k, or even open taxable brokerage account :).