5 GREAT REASONS TO LOVE HSA’S!

2022 contributions -$3,650/individual , $7,300 Couple and $1,000 catch up if over age 55

Qualifying High Deductible Health Plan (HDHP) annual out-of-pocket cannot exceed $6,900 for self coverage and $13,800 for family.

Link to HDHP video – High Deductible Health Plans (HDHP) With HSA!

SCHEDULE A ZOOM MEETING WITH BRAD:

Get more info today! Click below: You can reach me at brad@fortunefinancialgroup.com or website www.fortunefinancialgroup.com

Link to Deeper Dive into HSA video –

HSA Accounts – a Deep Dive Into Health Savings Accounts

How much can you contribute?

Who Can Use HSA’s?

What about the burden of having a high medical insurance deductible?

How does the money grow in a Health Saving Account?

Blog Post – Health Savings Accounts are Fantastic for Retirement!

Learn about best ways to invest money in 2018. And don’t forget to visit and learn more here:

Don’t Forget To Subscribe – …(read more)

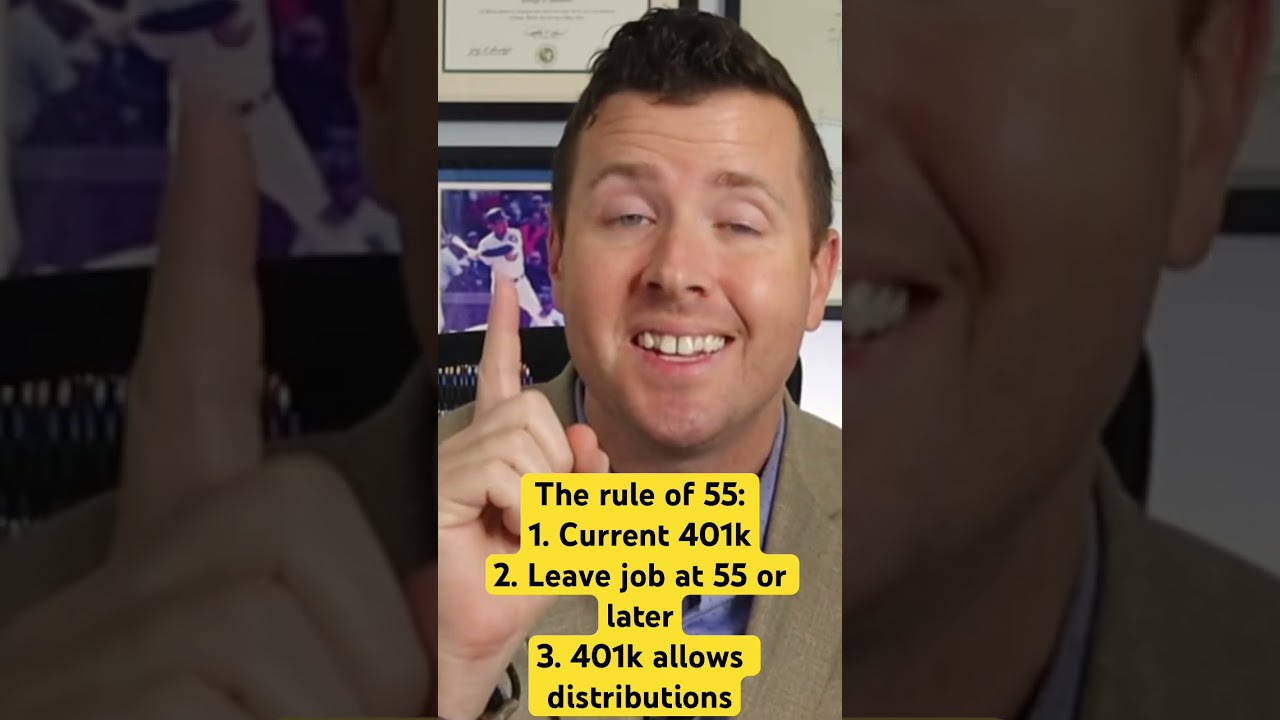

LEARN MORE ABOUT: 401k Plans

REVEALED: Best Investment During Inflation

HOW TO INVEST IN GOLD: Gold IRA Investing

HOW TO INVEST IN SILVER: Silver IRA Investing

When it comes to planning for retirement, many people look to traditional retirement accounts like 401ks. However, there is another option for saving for retirement that may be even better: Health Savings Accounts (HSAs).

An HSA is a tax-advantaged savings account that is used to pay for qualified medical expenses. Many people often overlook this account as just another expense and don’t consider it as a retirement account. However, if used properly, an HSA can be more beneficial than a 401k, especially for those who are young and healthy.

One of the biggest advantages of an HSA is the tax benefits it offers. Contributions to an HSA are tax-deductible, which means that individuals can reduce their taxable income by making contributions to their HSA account. Any earnings on the account, such as interest or investment gains, are tax-free as long as they are used to pay for qualified medical expenses. And withdrawals for any non-qualified expenses are taxed at the same rate as 401k withdrawals.

Additionally, an HSA can be used as a retirement account, while a 401k is only designed for retirement savings. Money in an HSA can be invested, just like a 401k, and allowed to compound over time. The difference is that HSA funds can be withdrawn tax-free, even after retirement, as long as they are used to pay for qualified medical expenses.

This is especially important as healthcare costs continue to rise, with the average retiree needing to budget around $285,000 for medical expenses during retirement. By having an HSA that has been allowed to grow, individuals can have peace of mind knowing that they have funds set aside specifically for healthcare expenses in retirement.

Another advantage of an HSA is its flexibility. Unlike a 401k, individuals can withdraw funds from their HSA at any time, for any reason. While individuals will have to pay taxes and possible penalties for non-qualified withdrawals, they still have more flexibility and control over their money.

Furthermore, HSAs offer portability, meaning the account remains with the individual regardless of job changes or retirement. On the other hand, with a 401k, an individual has to rollover their funds to a new employer or an IRA.

Overall, the decision to use an HSA over a 401k will depend on an individual’s financial situation, health, and retirement goals. However, for those who are young and healthy, an HSA can be a valuable asset for retirement planning, offering tax benefits, flexibility, and portability that a 401k does not. As a Certified Financial Planner, I highly recommend incorporating an HSA into your retirement planning strategy and maximizing its potential benefits.

Thanks Brad~ You're right, like a Super IRA – we have also referred to them as better than a triple-tax-free 401k – If you get a chance we have invented a Venmo for HSAs called HSAPAY – we were recently featured on LoupFunds (VC company) investment blog detailing what we are doing to help people save into their HSA. Thanks Brad for holding it down in HSAs! ~Craig

I still don’t understand how this is better than 401k which is also not taxed. Idk about other companies but from my understanding my company and all invest our 401k in stocks. Other than you can take the money out of HSA for health bills I don’t understand how it is so much more profit

does medical cannabis qualify ?

And if you use a FSA, Flexible Spending Account, use can use that to pay medical expenses making them all tax deductible. If you exceed the FSA you can pay medical bills with a points based or refund credit card.

Oh please answer this question I have been searching for and confused. I am getting mixed answers about reaching age 65. So when you reach age 65 you can use the HSA for non medical purchases and not get taxed or penalties?

Because there is no time limit on when you can refund yourself, technically the HSA balance when you retire could be used to pull out income in the amount of your medical expenses over your life time.. tax free, if you were a very detailed book keeper!

I always wait for your videos as they are so informative and effective. Thank you for always sharing the correct information. Keep posting.

Great info Brad and well explained. My ears PERKED up when you mentioned you can place it in a brokeage account to help grow this tax free . My question ( I don't live in your home state ) is there other brokeage company's besides TD that do this ?

Hi Brad, can someone who ChampVA and I have private overseas health insurance open a HSA? I am living overseas. Not planning on using HSA whiling living overseas just to invest.

I currently have a HDHP plan with an HSA. BCBS keeps getting too expensive. Can I keep contributing to my HSA if I switch to MediShare?

Thanks for the information. I'm getting ready to set up an account. So as you said, you don't pay the penalty for non-qualified expenses when you're 65 years or older. Do you pay income tax on the money you spend on non-qualified expenses when you're 65?

I have maxed out my HSA and Roth now. I’m an intern so i don’t have a 401k yet. Is there anything else out there??

I have one through my job. Can I still do these things with that?

wow you are good looking. Anyhow the only bad thing about HSA is something I encountered helping a neighbor. The HSA, despite it being designated for certain medical expenses, disqualified her for medicaid to pay for her part b each month thru a medicare savings program. If she had used that money towards a traditional 401k, this wouldn't be an issue. Probably a very narrow population of folks

Jokes aside, this is a great vid. Have been pumping up my HSA for years especially with employers matching funds.

I would hope you could elaborate on the over 65 no penalty comment near the end of the vid. Didn't know HSA money's could be used on non-qualified expenses. Thanks.

Thank You. I was totally clueless

I think HSA is the best account ever for its tax benefit but here would be my priority, assuming I have employer match contribution benefit

1.- contribute to your 401k up to the amount of your employer contribution.

2.- the move your contribution to HSA up to the limit amount.

3.- go back contribute to your 401k plan

You mention if you over 65 you can use it for any reason it doesn’t have to b medical related

How does the money grow ?. I don't see mine growing.

Is income that's deposited in an HSA , social security tax free?

Thanks for the video! Does the growth have to be used for medical or just the principal?

Nothing says safe money like Sheboygan Wisconsin lol

I fully fund my HSA. I’m a very healthy individual now, but hoping to defray the costs of medical expenses later.

Brilliantly explained. Thank you so much!

One really good thing about the HSA is that if you find yourself unusually healthy in retirement, you can still use the money for your Medicare Part A, B, C, and D or any other health insurance or dental insurance except medi-gap at age 65 or later tax free and penalty free. You also can use it for the 18 month COBRA insurance coverage if you quit your job at some point, also tax free and penalty free. The only gotcha's I can think of is if you die with the HSA and your beneficiary is not a spouse, the entire balance becomes taxable in a single year…the other potential gotcha is if you end up in a foreign country, that country probably will not recognize the HSA as being a tax free account.

I've watched almost all your videos and thank you! Do you still recommend HSA Bank or another now?

I don understand why they say veterans cant use this fund when the VA dont treat all medical issues and ant you yo go to outside doctor's beaus they cant handle the medical issue or you down meet the veteran percentage to be eligible either way this messed up for veteran beaus I need to have surgery.

Another important consideration is to look at how much your employer matches for HSA & 401k. Always contribute atleast to max amount employer is matching. Its likely you should be doing both HSA & 401k if employer matches for both.

When I leave the company, can keep the money ?

HAS SUCK my wifes med are 14,000 $ a month i am going to haft to pay that or she not be able to walk

i had to take out a 2nd morge on my house to pay for them if i still had my PPO plan the co pay on her

meds would be 100$ for the meds she takes so tell me how that HSA are so Great ??? and can save me money

“I’m coming directly to you for ask a quick favor”…something is wrong with this guy’s brain Joe Biden.

Just to understand this correctly…You cannot take this money out prior to 65 unless it is for medical expenses? And, after 65 you can take it out for "whatever you want"?

Thanks Brad!

I'm about to open an HSA through my job at 31yrs old- never heard of this before. Couple questions. 1. Do you ALWAYS need to be enrolled in a HighDed.Plan. to contribute to an HSA every year- or just to start one, 2. Does anyone know how to connect money from HSA into brokerage account, take $ from brokerage account and invest in stock market? Mine will be through HealthEquity. Wish it was Fidelity, but I think its my employers choice. Thanks yall

My wife and I both have the same HDHP with an HSA option. Is it better to open one account for the both of us or two seprate accounts? It looks to be cheaper per monthly premiums to go separate and the deductible is half of what getting one together would be.

My wife fully funds her HSA up to the family maximum. One caveat, California and NJ do not allow you to deduct contributions and you have to pay taxes on earnings.

Is it true that you can save receipts from qualifying medical expenses, that you paid out of pocket, and withdraw funds from your HSA years later to cover those expense with no tax or penalties?

You can contribute upto 19k on 401k and only almost 2k on HSA. You should contribute in your 401k to get your employees match and also max out your HSA. You cannot compare apples and oranges

Brad, my employer has an HSA healthfund plan and they will contribute $500 to that account in which i can use. Can I transfer that $500 to my HSA account after I open it up?

Won’t I have to pay ordinary income taxes at age 65 or greater for non-medical expenses?

So it's a great tax shelter but is this just a simple savings account at very low interest or is the money being invested like a 401k or an IRA and does a company match my contributions?