Schedule a free virtual or in-person consultation by visiting

We are based in Knoxville and Chattanooga!

Would a Roth Conversion improve my tax efficiency? What happens if I run out of income before I run out of life? Will my spouse be ok? In this study, we’ll take a look at being 64, single, and retired with $1,800,000 in your 401(k). Should you convert to a Roth IRA?

0:21 Introduction

1:58 Disclaimer

2:14 Case Study

2:25 Plan for Everything

2:48 Current Situation

3:25 Roth Conversions

4:32 401(k) vs Roth IRA

8:43 Tax Brackets

10:10 Impact of RMDs

11:11 Starting Distribution Tax

11:56 How Much to Convert?

12:14 Medicare Part B and D

13:04 Conclusion

A successful retirement plan means having a clear and achievable plan for your taxes, income, investment, healthcare, and legacy. If you are missing a piece of your financial puzzle or just want a second opinion, contact us at 865-392-4260 or visit

Learn more by visiting our website:

#incomeplanning #retirementplanning #retirementincome #retirewith1.8M #retirementat64…(read more)

LEARN MORE ABOUT: IRA Accounts

TRANSFER IRA TO GOLD: Gold IRA Account

TRANSFER IRA TO SILVER: Silver IRA Account

REVEALED: Best Gold Backed IRA

As retirement approaches, one question that many people face is whether to convert their 401(k) to a Roth IRA. There are several advantages and disadvantages to consider, particularly if you are single, retired, and have amassed a significant amount of retirement savings, as in the case of someone who is 64 years old with $1,800,000 saved.

First, it’s important to understand the difference between a traditional 401(k) and a Roth IRA. With a traditional 401(k), contributions are made with pre-tax dollars, meaning that the money grows tax-deferred but is taxed when you withdraw it in retirement. On the other hand, with a Roth IRA, contributions are made with after-tax dollars, and the money grows tax-free, meaning that there are no taxes to pay when you withdraw it in retirement.

One advantage of converting to a Roth IRA is that you can potentially save a significant amount of money on taxes in the long run. Because the money in a Roth IRA grows tax-free, you won’t owe any taxes when you withdraw the money in retirement, regardless of how much it has grown. This can be especially beneficial if you expect to be in a higher tax bracket in retirement, as you can avoid paying taxes on the money at that time.

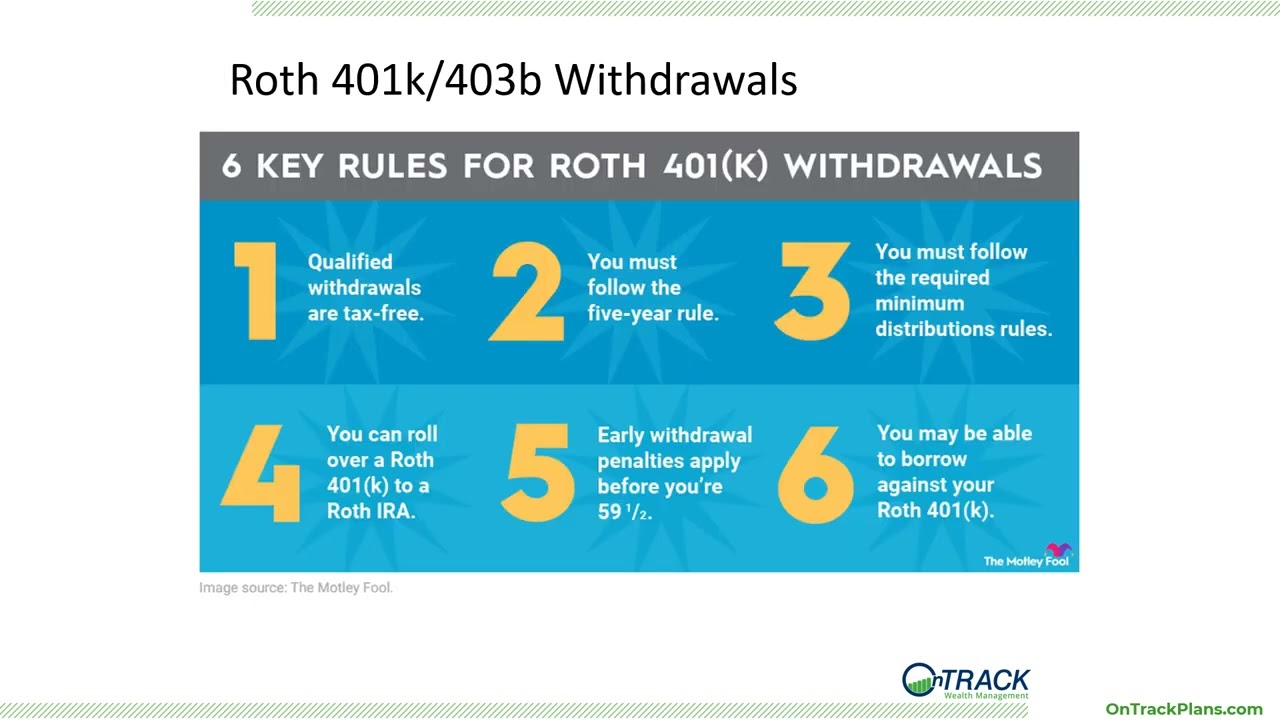

Another advantage of a Roth IRA is that there are no required minimum distributions (RMDs). With a traditional 401(k), you are required to start taking distributions at age 72, which can be a burden for some retirees. With a Roth IRA, you can let your money continue to grow tax-free for as long as you want, without having to worry about taking distributions.

However, there are also some potential downsides to consider when converting to a Roth IRA. One is that you will have to pay taxes on the amount you convert. This can be a significant amount, especially if you have a large 401(k) balance like the person in this example. You will need to carefully consider whether the tax savings over the long run are worth the upfront cost.

Another consideration is that once you convert to a Roth IRA, you cannot undo it. This means that if you change your mind later or if there are changes in tax laws that make a traditional 401(k) more advantageous, you won’t be able to switch back.

In the end, the decision whether to convert to a Roth IRA is a personal one that will depend on your individual circumstances and goals. However, if you have a significant amount of retirement savings and expect to be in a higher tax bracket in retirement, a Roth IRA may be worth considering. Additionally, if you don’t need the money immediately and can afford to pay the upfront taxes, a Roth conversion may be a smart move. Before making any decisions, it’s always important to consult with a financial advisor and carefully weigh the pros and cons.

I am 60 and single and plan to retire next year. RMD for me does not start until I am 75. I might not even be alive by then. I am in a 28 percent tax rate now. I think I will be in the same tax rate when I retire. So for me its a wash. I think I will just watch my investments grow and wait to see what happens. Thats 15 years from now before I have to worry about RMD. By that time my investments will easily pay for any taxes I have to pay. Worst case is I have to take RND, pay the taxes and reinvest the RMD.

Great info – thank you