Roth conversions have become a hot topic and for a good reason. After paying taxes throughout your working life, it would certainly be nice to strategically reduce taxes during retirement, if feasible. Nevertheless, the viability of a Roth conversion depends on individual circumstances, and after reviewing hundreds of Roth conversion plans, we’ve observed three primary reasons why a Roth conversion may be beneficial. In this video we’ll explore each of these reasons.

Want your own Roth conversion analysis? Find out more here

🔥🔥 Get the Ultimate Social Security Cheat Sheet! It takes the essential information from the 100,000 page Social Security website and condenses it down to just one page! 🔥🔥

Don’t miss my free online workshop, “How to Choose the RIGHT Age to File for Social Security.” In this workshop you’ll learn:

✔The Most Important Factors to Consider BEFORE You File for Benefits

✔How to Coordinate Your Social Security Filing Decision with Your Other Assets & Income for a Tax Efficient Distribution Strategy

✔Why This Is The Biggest Decision of Your Retirement

Access the workshop today at this link

➡️ Want to take a deeper dive into investment management and financial planning with Devin and his team? —

📊 Get a customized Social Security filing plan. Start with a 10-minute discovery call with a Registered Social Security Analyst

→ Financial Advisors! Become an RSSA and discover how Social Security expertise can unlock massive opportunities for your practice — 🧑💻

➡️ Get a copy of my newly revised book here —

➡️ Simple Questions? Join my FREE Facebook Group!

➡️ If your question is about the WEP/GPO, join this Facebook group instead

See Disclosures Below

⭐⚠️⭐Please read this⭐⚠️⭐

⚠️I am not an attorney, SSDI advocate, or affiliated with the Social Security Administration or any other entity of the US Federal Government . I am a practicing financial planner, but I’m not YOUR financial planner and since I don’t really know you, I can’t give you advice. So please don’t take this video as specific advice for your specific situation. Consult your own tax, legal and financial advisors. 🙇🙇🙇🙇🙇

—————————————————————————————————–…(read more)

LEARN MORE ABOUT: IRA Accounts

TRANSFER IRA TO GOLD: Gold IRA Account

TRANSFER IRA TO SILVER: Silver IRA Account

REVEALED: Best Gold Backed IRA

As retirement planning becomes more important than ever, many individuals are considering converting their traditional Individual retirement account (IRA) to a Roth IRA. A Roth IRA is a retirement account where individuals contribute with after-tax dollars, and the withdrawals made in retirement are tax-free. Below are three reasons why it may be worth converting to a Roth IRA:

1. Tax-Free Retirement Income

One of the primary benefits of a Roth IRA is the tax-free withdrawals. A traditional IRA is funded with pre-tax dollars, meaning that withdrawals made in retirement will be subject to income taxes. However, with a Roth IRA, the contributions are made with after-tax dollars, so you won’t owe any taxes on the withdrawals. This can be a huge advantage for those who anticipate being in a higher tax bracket in retirement, as they can avoid the higher taxes they would face with a traditional IRA.

2. No Required Minimum Distributions (RMDs)

Another benefit of a Roth IRA is that there are no required minimum distributions (RMDs), unlike traditional IRAs. RMDs are mandated withdrawals that must be taken from traditional IRAs starting at age 72. With a Roth IRA, you’re free to leave your money untouched for as long as you like, which can give you more flexibility and control over your retirement savings.

3. Estate Planning

A Roth IRA can also be advantageous from an estate planning perspective. Roth IRAs don’t have RMDs, as mentioned earlier, which means that they can continue to grow tax-free throughout your life. This can make them an excellent option for transferring wealth to your heirs, as they can inherit a tax-free asset. Additionally, a Roth IRA can be passed down to your beneficiaries without any tax liability on their end.

In conclusion, converting to a Roth IRA can be a smart move for those looking to maximize their retirement savings and minimize their tax liability. The tax-free withdrawals, no required minimum distributions, and estate planning benefits make it a compelling choice for many individuals. However, it’s important to consult with a financial advisor before making any decision to ensure that it aligns with your long-term retirement goals and overall financial plan.

Thanks, Devin!

I am of the belief, that the entire tax system will undergo a dramatic transformation for the better. All the resources spent on attempting to shelter income and figuring taxes, will be a thing of past.

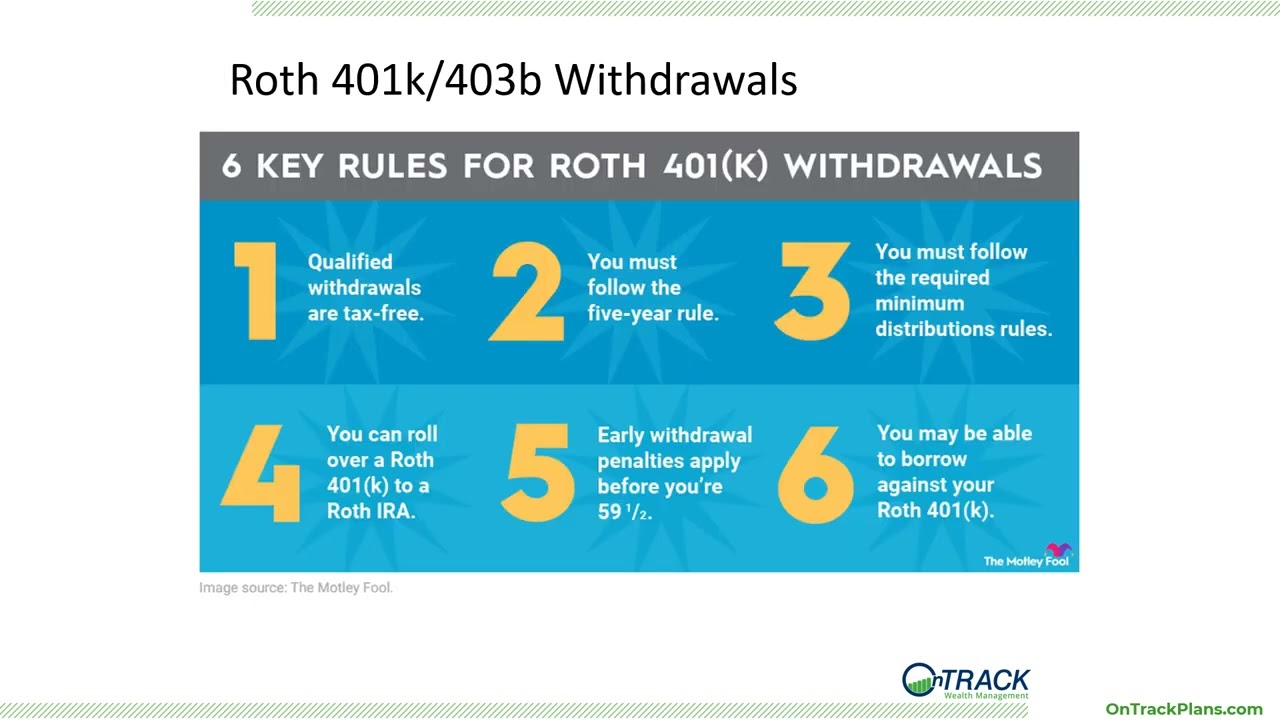

I've watched several videos about Roth IRA's and I just recently found out you can't touch that money for five years. I might have done things different had I known that little tidbit.

So paying the taxes from outside the Traditional IRA is best if possible. But what about paying with $ from inside the IRA?

Another reason to consider some Roth conversions would be if you are expecting an inheritance that consist of a pre tax account

You only have 10 years to spend /convert the inheritance money and if you are nearing retirement this can limit your ability to do some tax planning

So any conversions you can accomplish before you receive the inheritance will go a long way in you retirement withdrawal/tax strategy.

Devin is correct that emotions influence a part of the decision to convert to a ROTH. When investing, I research balance sheets and try to look at the market intellectually and not emotionally. Very rewarding results. On the other hand, after running the numbers of ROTH conversions, I added to that my personal belief that taxes will increase and tax brackets may shrink during my retirement. Then I factored in the emotional: I don't want the government forcing me to take RMD's. To me, getting out from under Big Brother's thumb is worth venturing past the 'logical' numerical limit of conversions.

Great explanation. Thank you.

Just recently retired and unfortunately only about an eighth of my IRA money is of the Roth variety. Wish I would have transferred over earlier, but oh well. Anyway, in all my analysis, a Roth conversion doesn't make much sense. I'll revisit it, but for me, it doesn't produce much in tax savings (can cost more, actually). Indeed my own analysis suggests I reap the tax benefits of the Roth on the front end of my retirement.

what about converting the day AFTER I reach FRA and start my retirement

Never forget that LIFE is NOT A MATH problem!

A reason to go with the Roth, I never hear anyone mention, is that with Roth income in retirement, I am very low income on paper. The Roth income doesn't show up on my Adjusted Gross Income on taxes. I now qualify for multiple programs and tax breaks because many of them only look ay AGI on the 1040 form. Not all programs do that, but many do.

100k vs 300k in taxes….. what is the time value of money? Would love to convert to a point but have no confidence paying taxes now will avoid enough taxes in the future to offset the potential gains on the amount of taxes paid now. Might, but don't see any reasonable certainty that will be the outcome. It's an interesting dilemma. We've worked hard and saved and now the government has their hand out (actually in our pocket) continuously.

Roth withdrawls dont count toward your earnings limit for social security and you dont pay taxes on it as income either.

Crystal ball thinking is easy on one point. If China Joe gets re-elected you will have less money year over year going forward.

I am too close to getting my IRA tax free. Retired at 62 and stay within my limits. In other words live with less and still help family. Inflation does suck though!

Exactly, the laws have changed. This is one of the reasons I am moving all my pre-tax money to a Roth. One year at a time and keeping it under the IRMAA limits. I should have all the pre-tax accounts (7 figures) by the time I am 70. I am about ½ way there at this point in time. It will be a PITA for your heirs if they are doing well (6 figure jobs).

Once again, your valuable info has me, both excited and worried (in a good way). Info is power!!

I'm spending that pretax money as soon as I turn 55 years old. I don't want to die with too much of tax deferred money

The video link explains the odds of getting approved for social security disability under the age of 40 is very hard to get approved and even harder to stay on disability once approved by the social security administration approval board! Now saying that my disability is very unique situation do to my disability lol! Below is my thoughts and prayers i have! Hope this explains and everyone understands how our lives was dramatically changed by just one event and we survived by the grace of GOD and all gods children that was sent to assist us and continue to send to us as needed! Thank god and thank you all for everything you do no matter how small it is it helps! My life is a great example of your preying for us and it shows god is listening to those prayers! Be thankful and grateful for everything and everyone around you and everyone's life journey is unique and are examples to others rather good or bad the examples they are to others! Have a great day and be safe!

I was 38 years old when i was approve for my social security disability benefits do to my injuries of no eyesight and dramatic brain injury the social security representative told us the odds of reviewing my eligibility is very slim! I will remain on disability until i turn 67 years old which i be swapped over to my social security retirement benefits. That means i will be on social security disability benefits for 29 years and if i live to my average family lifetime of age 88 years old i would been claiming social security benefits for 50 years if i live that long. It is crazy to think about a individual living on social security for over 30 years and insane to think of a individual claiming benefits over 50 years. It is remarkable i am alive after the home invasion that ended my career and took my eyesight and this the result of that event. Living in total darkness and everything and everyone is invisible to me until I touch or hear something. I am thankful and grateful i am alive and i can still perform task like electrical, mechanical, welding, woodworking, and use technology and tools that have been developed for me to preform those tasks. I continue to prey and hope the bionic eye is finally ready and i can get the funds to do the medical treatment to receive the bionic eye! I also pray the robotic guide dog is finally finished and released to the blind community and i have the funds to get one if i do not get the bionic eye before the robotic guide dog is available! In this I pray Amen! Be safe and enjoy the little things in life! 1:03

Taxes are lower than ever and national debt is higher than ever.

Three reasons for me. 1. Widow trap. 2. Keep taxable income down once I start collecting SS. At FRA, most of our expenses will be covered by SS. 3. Inheitence. Much easier to leave to kids than an IRA.

Don't optimize on reducing your tax payments. Optimize on the Post tax value of your assets.

When I start to get my first Social Security at the age of 62 will Social Security want to know if I have a Roth IRA and a Roth 401(k)? If so, will they tax my Roth 401(k) and or Roth IRA?

Another reason to convert to Roth is to protect a spouse from the “widow(er)’s tax trap” whereby one spouses passing causes 1 social security check to be lost, the standard deduction to be halved and the thresholds in tax brackets to lower dramatically. Additionally IRMAA thresholds for single taxpayers are also lowered as you mentioned. At the same time, RMDs would remain at the same level. Roth conversion can help alleviate some of the tax burden when the surviving spouse is at their most vulnerable.