You can now use your Roth IRA as an emergency fund, but should you?

Have a question you want to be answered on the show? Call or text 574-222-2000 or leave a comment!

Want to speak with a Certified Financial Planner™? Visit or call 574-247-5898.

Find more information about the Wise Money Show™ at

Be sure to stay up to date by following us!

Facebook –

Instagram –

Twitter –

Want more Wise Money™?

Read our blog!

Listen on Podcast:

Subscribe on YouTube:

Mike Bernard, CFP® offers advisory services through KFG Wealth Management, LLC dba Korhorn Financial Group. This information is for general financial education and is not intended to provide specific investment advice or recommendations. All investing and investment strategies involve risk including the potential loss of principal. Asset allocation & diversification do not ensure a profit or prevent a loss in a declining market. Past performance is not a guarantee of future results….(read more)

LEARN MORE ABOUT: IRA Accounts

TRANSFER IRA TO GOLD: Gold IRA Account

TRANSFER IRA TO SILVER: Silver IRA Account

REVEALED: Best Gold Backed IRA

Should You Use Your Roth IRA as an Emergency Fund?

An emergency fund is a crucial component of financial planning, providing a safety net during unexpected events like job loss, medical emergencies, or major repairs. It is recommended to have three to six months’ worth of living expenses set aside in a liquid and easily accessible account. However, some individuals may be tempted to dip into their retirement savings, such as a Roth IRA, when faced with emergencies. But is it a good idea? Let’s explore the pros and cons of using your Roth IRA as an emergency fund.

First, let’s understand what a Roth IRA is. A Roth IRA is an individual retirement account that allows individuals to contribute after-tax income, grow it tax-free over time, and withdraw it tax-free during retirement. Unlike a traditional IRA, contributions to a Roth IRA are not tax-deductible, but the earnings and withdrawals can be tax-free if certain criteria are met.

The main advantage of using a Roth IRA as an emergency fund is its flexibility. Contributions to a Roth IRA can be withdrawn at any time, penalty-free, as they have already been taxed. This means that in case of an emergency, you could access your contributions without paying a penalty or additional taxes.

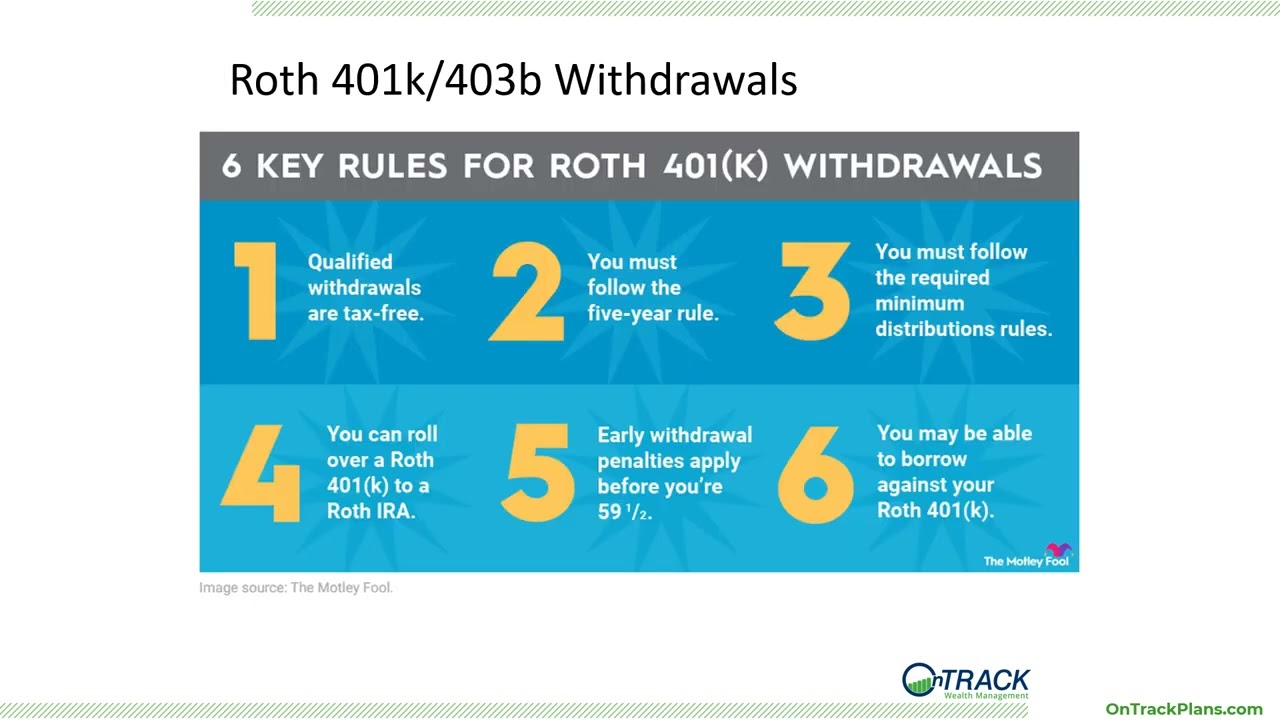

Moreover, if you have been contributing to your Roth IRA for several years, it is likely that the account has accumulated earnings. You may withdraw your earnings tax-free after reaching the age of 59 ½ or in specific situations, such as buying your first home or funding higher education. However, if you use your Roth IRA for purposes other than these qualified distributions, you will face a potential tax liability on the earnings withdrawn.

On the other hand, there are several reasons why using your Roth IRA as an emergency fund may not be recommended. Firstly, withdrawing from your Roth IRA permanently reduces the amount of funds available for your retirement. This could significantly impact the growth potential of your account, potentially jeopardizing your financial security in old age.

Moreover, your Roth IRA may have been invested in the market, and selling investments during a market downturn or when prices are low could result in substantial losses. Taking funds out of your Roth IRA during a market low means selling investments at unfavorable prices, missing out on potential gains when the market recovers. It is crucial to have a long-term investment strategy and not make impulsive decisions based on short-term emergencies.

Another drawback of relying on your Roth IRA as an emergency fund is the contribution limit. Contributions to Roth IRAs are currently limited to $6,000 per year (or $7,000 for individuals aged 50 and above) in 2021. If you withdraw a significant portion of your contributions, it may be challenging to replenish the account to take full advantage of tax-free growth over time.

In conclusion, while using your Roth IRA as an emergency fund may seem like a viable option due to its flexibility, doing so should be approached with caution. It is essential to evaluate the potential long-term consequences, such as losing out on retirement savings and missing out on market gains. Ideally, individuals should maintain a separate emergency fund outside of their retirement accounts to ensure they are adequately prepared for unexpected events while preserving their retirement savings.

Months 1-3 of a emergency fund should be in a cash account

Months 4-6 are okay to be in a ROTH;

Conflating between two types of emergencies: run of the mill daily-monthly bumps on road of life 'emergency' versus siren song 6+ month emergency fund for 6 month job loss or the like. Inasmuch as an Emergency Fund is type of insurance an individual may never need or use, Roth IRA can double as EF. Let's say someone with $52,000 salary wants 6 month $26,000 EF and can afford to devote only $6,500 year to either EF or Roth IRA. So after 4 years either $26k EF in Taxable Account or $26k Roth IRA: If there's $26k emergency then both EF & Roth IRA will work; but if none occurs then EF in TA owed taxes every year and can never contribute to Roth IRA for last 4 year; EF Roth IRA incurred no annual taxes. In year 5 person with EF in TA starts their first $6,500 Roth IRA while the EF Roth IRA contribution is $32,500.