Roth IRA vs 401k vs Individual Brokerage. The pros and cons of each account and how to choose which one to invest in first!

Between the Roth IRA, 401k and Taxable Brokerage account there are a number of things to consider. Tax benefits, income limits, limits on how much money you’re able to contribute, and restrictions on how and when you’re able to access your money! I’ll help you sort through all those details and decide which account to put money into first and whether or not you even need to open all of these investment accounts.

Invest in Bitcoin on Coinbase and get $10 in FREE BTC

Get Hilarious Investing Themed Merch –

If you enjoy my work and want to support the channel through Patreon you can do so here:

WATCH NEXT:

✅ Should I Contribute to a 401k With No Match?

✅ Roth IRA vs Traditional IRA vs 401k

✅ The Five Investment Accounts Everyone Needs

– I Recommend Investing at These Brokers-

✅ M1 Finance –

✅ Charles Schwab –

✅ Fidelity –

✅ TD Ameritrade –

– Connect with Me On My Socials –

Instagram:

Facebook:

Twitter:

Join my NEW Facebook group for investors:

Music in all my videos via Epidemic Sound:

#rothiravs401k #investmentaccounts #wheretoinvest

A bit about my credentials…I have a B.S. degree in Finance, I’ve spent my entire career working in various corporate finance roles, and have been an active stock market investor for over 20 years. While all of this means I know what I’m talking about (most of the time!), it does not mean you should act solely on my word alone.

I am not intending to, nor licensed to give personalized financial advice. I’m merely trying to share my knowledge and experience so that you are able to make better financial and investment decisions for yourself based on your own research!

Put another way…

DISCLAIMER: Jay Fairbrother, including but not limited to any guests appearing in his videos, are not financial/investment advisors, brokers, or dealers. They are solely sharing their personal experience and opinions; therefore, all strategies, tips, suggestions, and recommendations shared are solely for entertainment purposes. There are financial risks associated with investing, and Jay Fairbrother’s results are not typical; therefore, do not act or refrain from acting based on any information conveyed in this video, webpage, and/or external hyperlinks. For investment advice please seek the counsel of a financial/investment advisor(s); and conduct your own due diligence.

AFFILIATE DISCLOSURE:

This description contains affiliate links that allow you to find the items mentioned in this video and support the channel at no cost to you. However, this DOES NOT impact my opinions and comparisons. Thanks for your support!

…(read more)

LEARN MORE ABOUT: IRA Accounts

TRANSFER IRA TO GOLD: Gold IRA Account

TRANSFER IRA TO SILVER: Silver IRA Account

REVEALED: Best Gold Backed IRA

When it comes to retirement planning, there are a variety of options to consider. Two of the most popular types of accounts are 401(k)s and Roth IRAs. But what about taxable brokerage accounts? Which should you prioritize?

A 401(k) is an employer-sponsored retirement plan. It allows you to contribute pre-tax money to an account, which will then grow tax-free until you withdraw the money in retirement. Your employer may even match your contributions, which is an added bonus.

A Roth IRA is a retirement account that allows you to contribute after-tax money and grow it tax-free. The money can be withdrawn tax-free in retirement, and if you follow the rules, you can avoid paying taxes on the money.

A taxable brokerage account is a type of investment account that does not offer the same tax advantages as a 401(k) or Roth IRA. You will have to pay taxes on any gains or income that you receive from the account. However, it can still be a useful tool for retirement planning.

So which should you prioritize? The answer depends on your individual financial situation. If you have the option to contribute to a 401(k) with an employer match, that should be your first priority. If you don’t have access to a 401(k), then a Roth IRA should be your next priority. Taxable brokerage accounts can be a good way to diversify your investments, but they should not be your primary retirement savings vehicle.

Ultimately, the best retirement plan is one that is tailored to your individual needs and goals. Consider all of your options and prioritize the ones that make the most sense for you.

WATCH NEXT -> The 5 Investment accounts everyone should have https://youtu.be/D4yjBYq4X8k

401k proceeds will be taxed as regular income when you withdraw. So just as if you are taking a paycheck from your own money the government wants its cut. On the flip side of that a standard brokerage account will be filled with already taxed money so you have the opportunity to pay 0% taxes on your gains as a Long term capital gain from brokerage accounts is TAX-FREE up to 85K / year. This Is HUGE as in a 401k you are taxed on the whole dollar amount not just the gains and there is no option to pay 0% taxes.

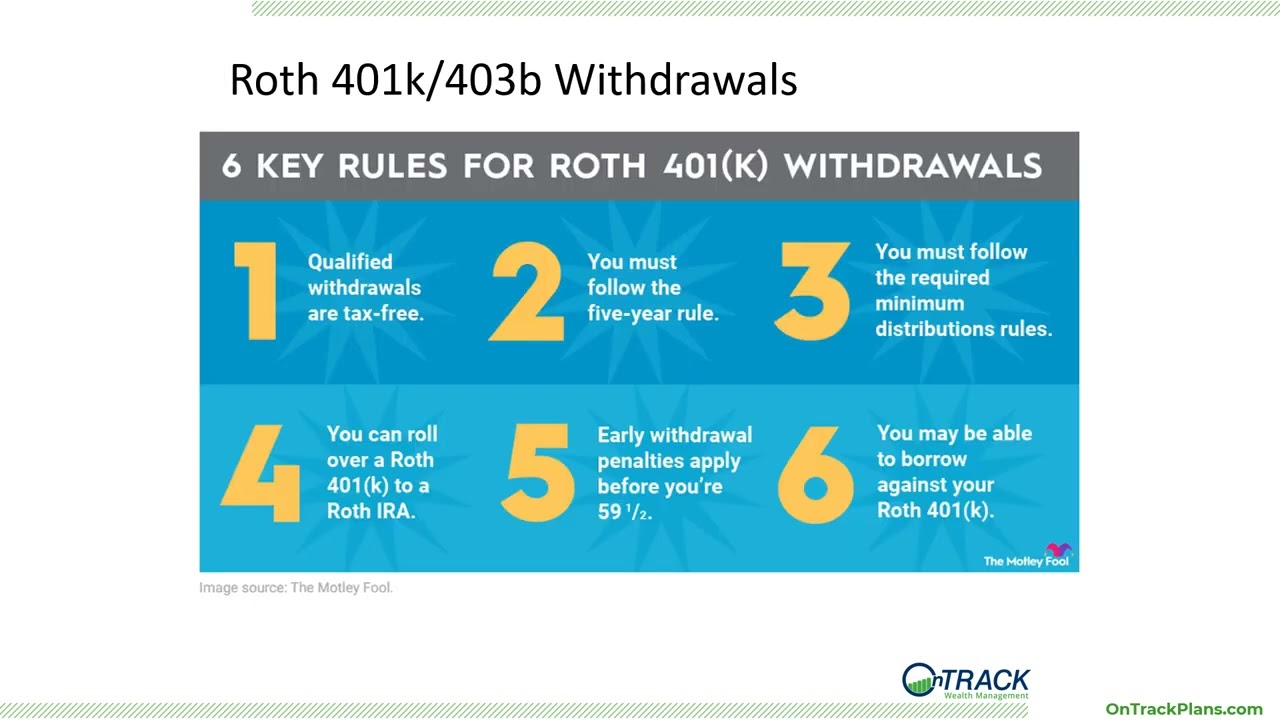

FYI, 401K also has a ROTH version

A good option would be to contribute to your ROTH 401K after you have maxed out the ROTH IRA. When you retire you can roll that ROTH 401K into your ROTH IRA which could really help get around that $6000/year contribution limit on a ROTH IRA. I would do half ROTH 401K and half pretax 401k contributions to tax advantage of the tax deferred benefits.

What if your 401k is charging 1.6% in fee's you'd be better off throwing that money into a taxable account instead and buying into a tax efficient ETF like Vanguard SP500 index fund (ticker VOO) that only charges .03% in fee's…over a 30 year period tell me where the real advantage is now between a 401k and taxable brokerage account…i think some 401k's charge obscene fee's that actually put you at a disadvantage,,correct me if im wrong.

"you're not getting any tax advantages with the traditional brokerage account"

On the contrary, long term capital gains tax rates from a brokerage account are lower than the marginal tax rate that you would pay when you withdraw from a 401k. Depending on how much you withdraw annually, you may end up paying double the tax on a 401k withdrawal vs a similar amount being pulled out of a brokerage account. This can amount to tens of thousands of dollars annually in taxable savings.

Do companies match for roth ira/tsp?

Hi Jay

Im hoping you van one day make a video on bonds . I’m close to the age of 50 and it’s time for me to start putting money into bonds . Just don’t know what type of bonds and what to look for when it come to investing in bonds . And what kind of return I should expect.

Great video! But wonder why you did not mention HSA max out after 401K employer match and ROTH IRA max out ?

Awesome. I’ve got a rollover IRA that I’m contributing into. Is that good ?

Please go over S&P Fund

Great video, super comprehensive!

It's so annoying, why do they limit the number of choices in those employer sponsored funds? I was really surprised how few choices my 401K had available.

Nice sharing

Stay connected

I am with you Jay, I believe retirement accounts should come first either 401k or Roth IRA.

Great explanation of the 401k match! I agree with the prioritization order, but also like using a brokerage for far-off, but not too far-off goals, so wouldn't necessarily wait until my 401k was maxed (if I had one) to put money there. I like a little in everything with the big goals of maxing Roth and getting the employer match!

Funnily enough I'm in the process of looking at this for a UK equivalent, good advice Jay! 🙂

I actually still agree with your order even if you are looking to retire early as you can still access traditional 401k contributions prior to 59.5 without paying the 10% penalty via roth conversions. Yes you still will have to pay regular income taxes but you can still access your money prior to 59.5 if you choose to retire early