In this video we’re answering the question “What is the 5 Year Rule for Roth IRA and Roth 401(k) Contributions?” The White Coat Investor wants to help you stop doing dumb things with your money, so in this video series we answer questions you have submitted.

To get your questions answered by The White Coat Investor, visit and record your question.

The White Coat Investor has been helping doctors with their money since 2011. Our free financial planning resource covers a variety of topics from doctor mortgage loans and refinancing medical school loans to physician disability insurance and malpractice insurance. Learn about loan refinancing or consolidation, explore new investment strategies, and discover loan programs for specifically aimed at helping doctors. If you’re a high-income professional and ready to get a “fair shake” on Wall Street, The White Coat Investor channel is for you!

Subscribe Here:

Main Website:

Student Loan Advice:

Facebook:

Twitter:

Instagram:

Subreddit:

Online Courses:

Newsletter: …(read more)

LEARN MORE ABOUT: IRA Accounts

TRANSFER IRA TO GOLD: Gold IRA Account

TRANSFER IRA TO SILVER: Silver IRA Account

REVEALED: Best Gold Backed IRA

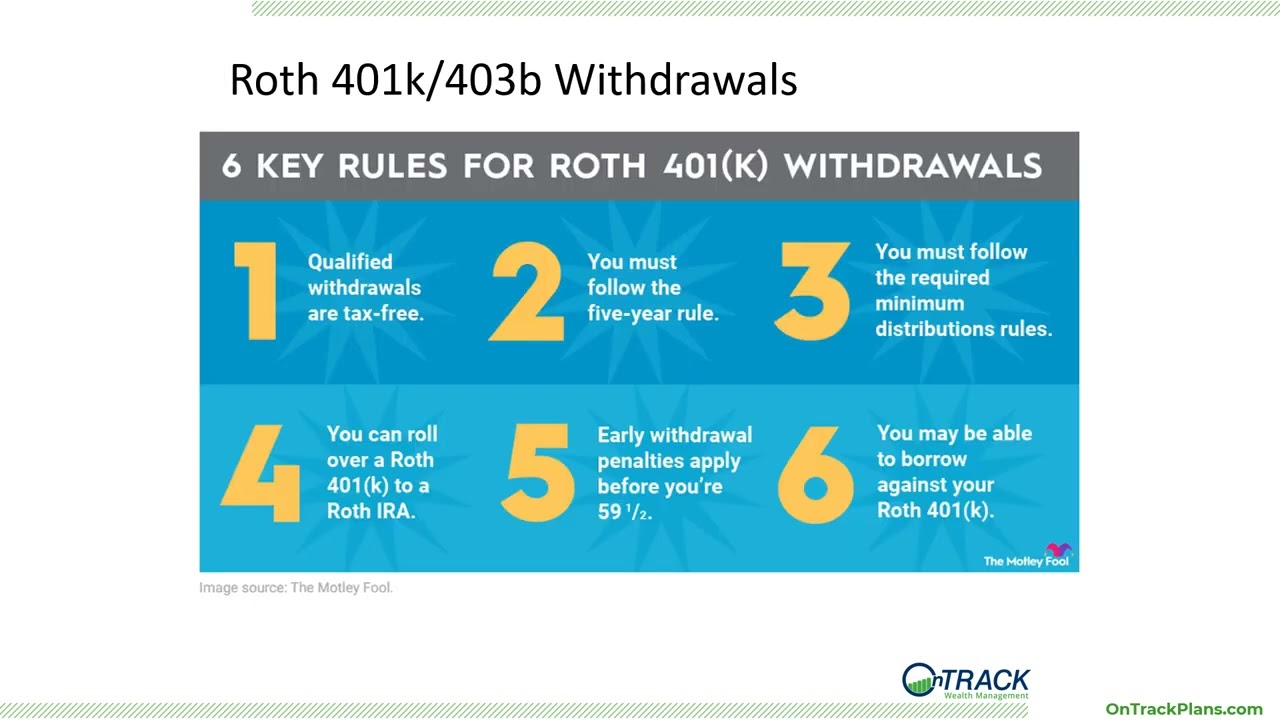

When it comes to saving for retirement, a Roth IRA (Individual retirement account) and Roth 401(k) are great options to consider. However, there are certain rules and regulations you need to follow when contributing to these accounts. One such rule is the 5 Year Rule for Roth IRA and Roth 401(k) Contributions.

The 5 Year Rule is pretty straightforward. It states that after you make your first contribution to a Roth IRA or Roth 401(k), you must wait a minimum of 5 years from the start of the tax year in which you made your contribution to withdraw any earnings or gains without penalty. This rule applies to both traditional Roth IRA and Roth 401(k) accounts.

Why is the 5 Year Rule important?

The 5 Year Rule is important because it impacts how you can access the money you contribute to your Roth account. Since Roth contributions are made after-tax, you can withdraw your contributions at any time without penalty. However, the earnings or gains on your contributions are subject to the 5 Year Rule. If you withdraw your earnings before the five-year waiting period is up, you could face a 10% penalty on top of taxes owed.

Exceptions to the 5 Year Rule

Like most IRS rules, there are exceptions to the 5 Year Rule. Here are a few instances when the 5-year rule may not apply:

– Qualified distributions: If you are over the age of 59 ½ and have held a Roth IRA account for at least five years, all distributions are qualified and tax-free.

– Disability: If you become disabled and are unable to work, the 5 Year Rule does not apply.

– Death: If you pass away, the 5 Year Rule does not apply for your beneficiaries.

– First-time home purchase: You can withdraw up to $10,000 of earnings without penalty to use for a first-time home purchase. However, the five-year waiting period still applies.

Key Takeaways

The 5 Year Rule for Roth IRA and Roth 401(k) contributions is a crucial factor to consider before contributing to these retirement accounts. The rule regulates when you can withdraw your earnings or profits on your contributions without a penalty. Be sure to understand the rule and know the exceptions to the rule to avoid facing penalties in the future. Investing in a Roth IRA or Roth 401(k) is a smart financial move, but you need to be aware of the rules to reap the full benefits.

0 Comments