In this episode, Laura Rotter of True Abundance Advisors discusses the importance of organizing retirement accounts and the ease of rolling over accounts from previous employers. She highlights common issues individuals face, such as leaving accounts with previous employers and losing login information, leading to a lack of awareness of their retirement savings.

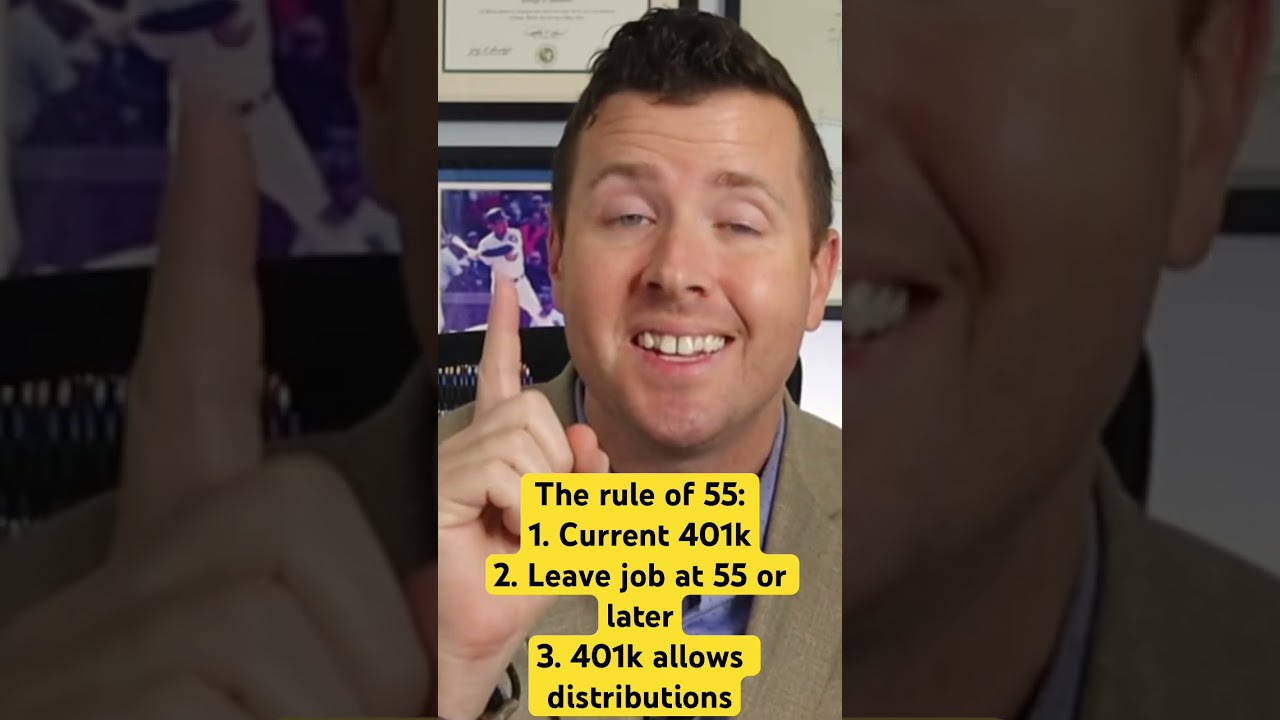

Laura explains the three choices individuals have when leaving an employer with a retirement account: leaving the account with the employer, rolling it over into a rollover IRA independently, or working with a financial advisor to facilitate the rollover. She emphasizes the simplicity of the rollover process, which typically involves contacting the 401k provider, filling out necessary paperwork, and ensuring any distributed funds are deposited into a new tax-deferred account within 60 days to avoid tax implications.

For those seeking assistance or guidance on retirement account rollovers or investment strategies, Laura encourages reaching out to her for support. She emphasizes the benefits of organizing financial life, including seeing all accounts in one place and ensuring investments align with individual and household goals.

Key Points:

– Many individuals have retirement accounts scattered among previous employers, leading to a lack of awareness of their savings.

– Options for handling retirement accounts when leaving an employer include leaving the account, rolling it over into a rollover IRA independently, or working with a financial advisor.

– The rollover process involves contacting the 401k provider, completing necessary paperwork, and depositing distributed funds into a new tax-deferred account within 60 days to avoid tax implications.

– Laura encourages seeking assistance for retirement account rollovers and investment strategies to organize financial life and align investments with goals.True Abundance Advisors does not warrant that the information in this video will be free from error. None of the information provided is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This information should not be relied upon for transacting securities or other investments. Under no circumstances shall True Abundance Advisors be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the materials provided. In no event shall True Abundance Advisors have any liability to you for damages, losses, and causes of action for accessing this video.

#retirementplanning #financialadvisor #financetips #finance #achieveyourgoals #trueabundanceadvisors…(read more)

LEARN MORE ABOUT: 401k Plans

REVEALED: Best Investment During Inflation

HOW TO INVEST IN GOLD: Gold IRA Investing

HOW TO INVEST IN SILVER: Silver IRA Investing

Leaving a job can be a stressful and overwhelming experience, especially when it comes to handling your retirement savings. One important decision you’ll need to make is what to do with your 401k account.

There are a few options available to you when it comes to your 401k after leaving your employer. The first option is to leave the money where it is. Most employers allow you to keep your 401k with them even after you’ve left the company. This can be a good choice if you’re happy with the investment options and fees associated with your current plan. However, if you’re looking to consolidate your retirement savings into one account, this may not be the best option for you.

Another option is to roll your 401k into an Individual retirement account (IRA). This can be a good choice if you want more control over your investment options and fees. With an IRA, you have a wider range of investment options to choose from compared to a 401k. Additionally, you may also be able to take advantage of lower fees and better customer service with an IRA.

You also have the option to roll your 401k into your new employer’s 401k plan. This can be a good choice if you’re happy with the investment options and fees offered by your new employer. Additionally, rolling your old 401k into your new employer’s plan can make it easier to keep track of your retirement savings and manage your investments in one place.

Finally, you can choose to cash out your 401k. While this may seem like an appealing option, especially if you need the money right away, it’s important to consider the potential consequences. Cashing out your 401k can result in hefty taxes and penalties, which can significantly reduce your retirement savings. It’s generally recommended to explore other options before resorting to cashing out your 401k.

Overall, the decision of what to do with your 401k after leaving your employer will depend on your individual financial goals and circumstances. It’s important to carefully consider all of your options and seek guidance from a financial advisor if needed. By taking the time to make an informed decision, you can ensure that your retirement savings continue to grow and support you in the future.

0 Comments