🤔Will taxes go up or down in the future? If you think up (like me) then my advice is to not put anything over matching into your 401K. Instead pay the taxes now and invest in a Roth IRA. And make sure you use a company that allows you to have the freedom to invest in whatever you want ✅

My goal is to change the way you think about money to help build you more wealth. Subscribe for more content like this!

🔥 The world we are going into is not the world we are leaving behind, need a guide? – Here’s How to Work With ME 🔥 —

➡️ Order “UnCommunist Manifesto” Here: go.1markmoss.com/uncommunist

➡️ INCREASE YOUR SOVEREIGNTY NOW: JOIN MY FREE NEWSLETTER HERE –

🔥 Don’t Worry About Taking Notes! You Can Get All My Slides and Resources!

Link to Learn More — 🔥

🔴(BEWARE OF SCAMMERS)🔴

They are impersonating me in the comments. My comments have a “checkmark” so look for that. Please beware, I will never message you asking you to give me money or to talk to me on WhatsApp. This is my only YouTube channel, and my social media platforms can be found below. 👇

___________________________________________________________________________________________

★☆★ CONNECT WITH MARK ON SOCIAL MEDIA ★☆★

Facebook ▶

Twitter ▶

Instagram ▶

LinkedIn ▶

____________________________________________________________________________________________

Disclaimer: I am NOT a financial advisor, and nothing I say is meant to be a recommendation to buy or sell any financial instrument. I will NEVER ask you to send me money to trade or invest for you. Please report any suspicious emails or fake social media profiles claiming to be me. Don’t invest money you can’t afford to lose. There are no guarantees or certainties in trading or investing. My videos may contain affiliate links or sponsorship to products I believe will add value to your life and help you. In some cases, I may receive payment or other consideration from the companies mentioned in the videos. No matter what I or anyone else says, it’s important to do your own research before making a financial decision. SEE FULL DISCLAIMER HERE: …(read more)

LEARN MORE ABOUT: 401k Plans

REVEALED: Best Investment During Inflation

HOW TO INVEST IN GOLD: Gold IRA Investing

HOW TO INVEST IN SILVER: Silver IRA Investing

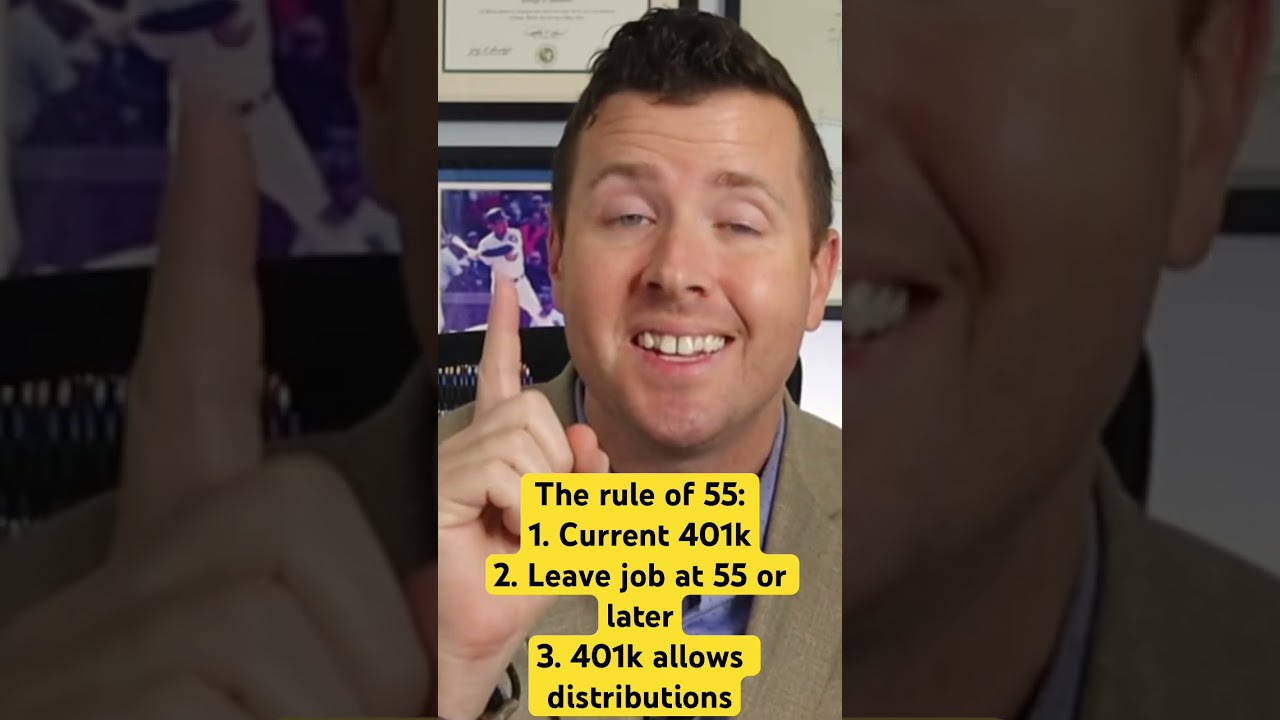

Stop Putting Money into Your 401K! (Here’s Why)

For years, the 401K has been touted as the go-to retirement savings plan. Employers often encourage their employees to contribute to a 401K, offering matching contributions to sweeten the deal. However, it might be time to revisit this conventional advice and consider alternative avenues for retirement savings. Here are a few reasons why you should stop putting money into your 401K.

Limited Investment Options

One of the major drawbacks of a traditional 401K is the limited investment options it offers. Typically, these plans provide a few mutual funds or target-date funds to choose from. This lack of variety means you are subject to the performance of those funds, limiting your ability to diversify your portfolio and potentially limiting your returns.

Furthermore, the fees associated with managing these funds can eat into your savings over time. While the fees may seem insignificant at first, they can add up significantly over the course of your career. These expenses can be avoided or reduced by exploring other investment options outside of your 401K.

Lack of Control and Flexibility

Another issue with the 401K is that it restricts your control and flexibility over your investments. You are limited to the options provided by your employer, leaving you in a passive position when it comes to managing your retirement funds.

Investing in alternative vehicles, such as an Individual retirement account (IRA) or a brokerage account, gives you greater control over your investment choices. With these options, you can choose from a wide range of investment opportunities and adjust your strategy as needed. This control and flexibility can be vital when adapting to changing market conditions or personal financial goals.

Penalties and Restrictions

While the 401K is designed to incentivize long-term retirement savings, it comes with costly penalties and restrictions. If you need to withdraw funds from your 401K before the age of 59 ½, you’ll typically face a 10% early withdrawal penalty, in addition to income taxes on the amount withdrawn. This limitation can hinder your ability to access your money for emergencies or other financial needs.

Alternatively, investing in non-retirement accounts allows you to access your funds without penalties or restrictions. While it’s important to have discipline and not tap into your savings impulsively, having the option can provide peace of mind and financial security in uncertain times.

Diversification and Potential for Higher Returns

Lastly, diversification is key to maximizing investment returns and reducing risk. By solely relying on a 401K, you may miss out on other investment opportunities that could potentially boost your returns over time. Diversifying your investments across various asset classes, such as stocks, bonds, real estate, or even starting your own business, can enhance your financial position and offer potential for higher returns.

Of course, it’s essential to consult with a financial advisor or do thorough research before making any major investment decisions. They can guide you through the process, help evaluate the risks, and determine the best strategy based on your unique circumstances and goals.

In conclusion, while the 401K has long been the default retirement savings plan, it’s worth reconsidering whether it’s the best option for you. Exploring alternative investment vehicles that offer more control, flexibility, and potential for higher returns can provide a more personalized and diversified approach to securing your financial future. Ultimately, the decision should be based on your specific financial situation and goals, ensuring a sustainable retirement plan that suits your needs.

I love this guy and all his knowledge

Not a fan of 401ks. You have to wait til your 60 something in order to "enjoy" it. No thanks. I'd rather find better things to bring in immediate passive income than sit and wait for xx years.

Mark what about your employer is matching your roth 401K?

Roth 401ks solve this

Another plus for the after tax bucket and mega backdoor roth conversions

Thoughts on buying gold and silver within the 401k? I keep seeing advertisements about this.

ALERT: Bad Advice! You can have a Roth 401k where you don't take a tax deduction now, but it is 100% TAX FREE when you make withdrawals after age 59 1/2

So I suppose a SEP ira is a bad idea too??

I put in only up to the match amount. I'd rather have control over my own investments.

Unless 401ks become gold, silver or bitcoin optioned, what's the point? You're putting in worthless fiat, getting matched with more worthless fiat by your employer, and it is inevitably going to 0 sooner rather than later thanks to this cabal

I’ve found that the investment options in 401k’s are atrocious. They are curated to maximize profits for the 401k company—not you. I’ve found them so bad, in fact, that I do better in my non-tax-deferred investment account than the 401k. I actually quit my job once—just so I could roll my 401k into my IRA to manage it myself with many more options and possibilities.

Also, 401k’s are denominated in dollars, so I believe they will likely lose much of your gains (or worse) to inflation and a worsening economy.

Ya no…with bitcoins upside potential its bitcoin or nothing

Pretty much going to Rebel Capitalist Live for a similar question. I’m 25 and just learning about this system. Do you do the 401 k and then make a Roth IRA. Or following some peoples models..? So many types of services and I don’t know where to start

It’s the easiest way to save for me so I’ll take my chances!

U forgot to mention what other places are better to put your money in? Can u make a followup video on the best investments to put your money in pls thank you'

First time I ever disagreed with you 100%. Roth 401k is a perfect rebuttal to your argument.

I think the bigger danger is that the 401k is an exception to the tax law, and can be changed with the stroke of a pen. It would be quite simple for the government to require 50% of 401k funds to be lent to the government (ie. "invested" in government bonds).

Meh! That`s a ridiculous statement. Put as much money in as many IRA`s and 401k`s as possible. You get gains on the deferred interest which is enormous over decades. Of course taxes will be higher. But that will be hugely offset by the gains realized on the deferred taxes. And lets not ignore the fact that most people will be in a lower tax bracket after retirement. Stupid statement, very bad advice

This is very dumb. 1. Roth 401k and 2. You still have to pay taxes on the money that you earn from investments outside of a Roth IRA.

Edit: I was wrong on this. 401k is takes as income and not capital gains.