My reaction to the CBS 60 Minutes Documentary: The 401k Fallout. As we head into a similar situation, it’s important to understand cyclical events so we can learn from the past. This happened back in 2008, its possibly happing now, and will happen in the future.

Each “EVENT” is different in its own way but the impact in the market and to people is still the same. The lack of financial literacy has gotten worse, not better. People are getting hurt in larger amounts and in bigger quantities as more people are getting into the market (including NFT’s and digital currencies.)

Original Documentary:

_____________________________________________________________

Do you want to be coached by me?

Checkout our Financial Literacy Course:

(USE COUPON CODE: 995OFF for your FREE course)

Are you interested in getting into the industry or looking for support?

Follow me on Social Media:

Instagram:

Facebook:

LinkedIn:

Video Editing:

Equipment:

Mic:

– Deity D3 Pro Microphone:

– Rode VideoMicPro Microphone:

Camera:

– Cannon G7x Mark III Camera:

– Cannon G7x Mark III Cold Shoe Mount:

– Cold Shoe Mount Extension:

Lighting:

– Godox SL-60 LED:

– Godox Softbox:

_____________________________________________________________…(read more)

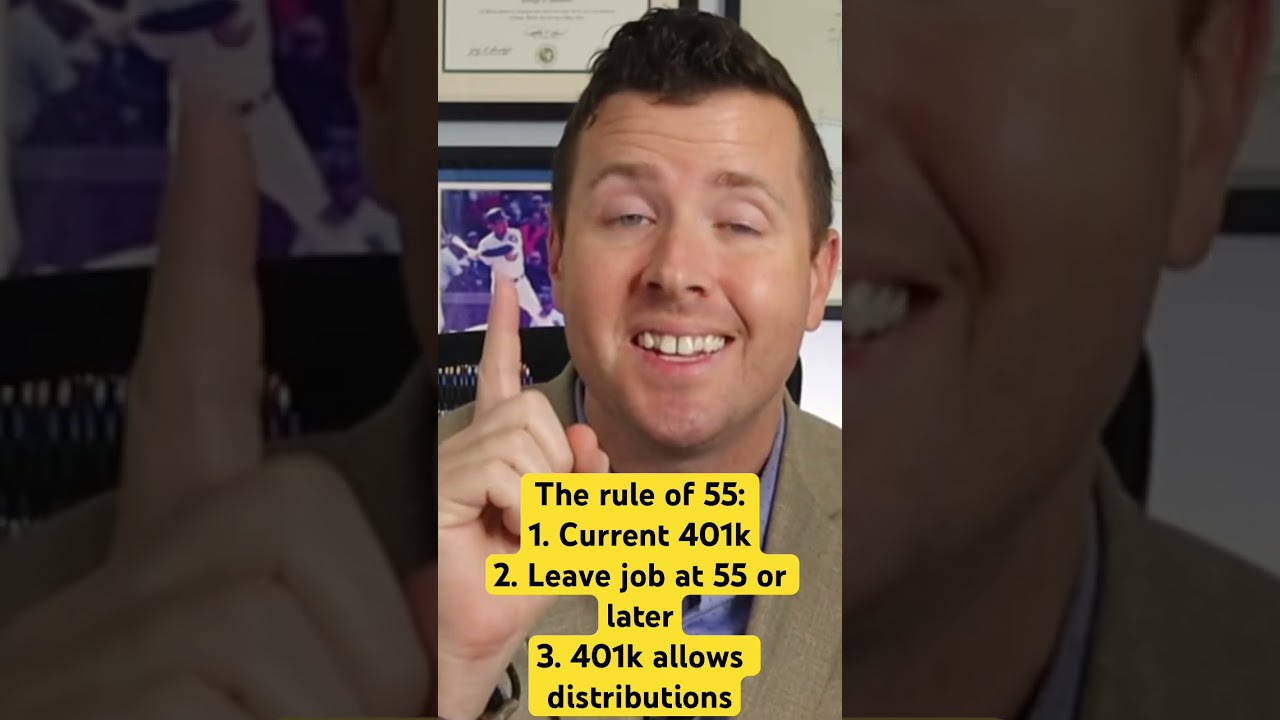

LEARN MORE ABOUT: 401k Plans

REVEALED: Best Investment During Inflation

HOW TO INVEST IN GOLD: Gold IRA Investing

HOW TO INVEST IN SILVER: Silver IRA Investing

Do people seriously not even scan the overview on the prospectus to look at the fees? It's literally the first thing I see – immediately followed by the long term performance then the fund composition. I'm no finance guy, I just like to know what I am getting into.

So across all my accounts, I'm down about $70k but it will come back. Even if it doesn't I'm still better off putting the money in the bank. Be less emotional about money – it's just a means to an end.

Glad I put all my 401k into a secured account.

Get a passport and bail out of the country. The next Recession will be One to remember. 401ks are worthless when the dollar has collapsed.

If there should be a change to the 401k I would like to have an option of a traditional 401k, a Roth IRA or a combination of both. The Roth IRA would not have a minimum distribution because the taxes have already been paid. I like that.

You are correct the mutual fund industry likes uninformed customers they can overcharge for underperforming.

Good news is there is a ton of information out there now on investing and the advantages of index funds. The Money Guy show has a lot of great videos here on YouTube.

Didn't the market bounce back in 2 years? And surpass its previous high in about 3 years?

401K=mutual funds=stock market casino=201K….

3 Trillion lost YTD in 401K/ IRAs Let's go Brandon!

So you re-played the video and repeat the same content

Did you educated?

Did you give other options?

Or did you just pointed the problem

I’m a dividend investor, my wife and I have invested in the s&p500, both through my TSP with the government and through fidelity in her 401-k. Cashed out 370k from the S&P and invested with a full service broker.. Until about 3years ago we were 100% in the s&p after over 30 years. I’m retiring at the end of the month at 59, while my wife will retire next year at 54. We currently have 5.7 million in out tex deferred savings.

100 minus your age = % in stocks/real estate/equities. There it is. . .financial planning to one simple equation.

That said, I remember reading an article years ago (many) of an 80 year old man who was still puttering at work and 100% in stocks and planned to be that way the rest of his life. It was an interesting story. He didn't really believe in traditional retirement and I guess was healthy enough he could keep working and enjoying it. He didn't get excited at the 40% drop in 2008. Interesting. . .I mean. . .how much can you spend at one time if you are working anyway? I still think about that once in awhile.

Another interesting factoid – robust middle classes tend to appear after pandemics. So. . .I am not sure the next market crash will equal a lot of layoffs although I imagine there will be job switching/scalebacks in hours.

This financial advisor has it together! I’m old, rich and this gentleman knows what he’s talking about.

Good analysis. But work on the sound quality. Sound quality on analysis videos like this are very important.

Interesting content, videos like this and analysis from a qualified personnel really helps.

I've never read a prospectus but I do plenty of research and I ask questions. Last year, when I saw the first signs of the stock market beginning to go down, I moved my entire 401k balance into a stable value fund (I had already researched what to do whenever I became concerned about my money). That was the best decision I could have made then. Instead of my account losing what probably would have been $40k or more in the market drop we're in now, my losses have been minimal. I just retired a month ago. I don't have so much in my 401k that I'll never need to earn any more money, but my mortgage is paid and I can do something part-time when I'm ready. I think it's very important to learn everything you can about your own investments and options. As one of the men in the video said, some of the funds in 401k plans are not good so you have to do your research.

First, let's start by understanding how much the fees are for the plan. How do we find that out?

There are thousands of books in the library and thousands of YouTube videos to teach you. Just turn off the TV and put a few hours a month into educating yourself.

It’s not that complicated.

What we see is intentional to break workers and help reset for the government and corporations.

Reallocation is the key. I'm turning 51 next week and intend to retire at 58. Once this market turns around in a few years, I'm going to be moving to a more conservative allocation. I'm also buying things like I- bonds to help keep things secure. Great video, by the way!

I love the downturn, stocks on sale, time to rebalance your Investment. Still up by 40% since I retired 6 years ago.

2008 prepped me for what we have going on today. I hope.

The 60 minutes piece says it all , clearly without any explanations needed ,401k s are managed with fees , statement of fact , “management fees dwindle the savings in 401k plan up to half of its savings by half its value over 30 years . It’s a swindle

Keep your money away from Wall Street genies in a bottle, 401ks and how they were conjured into existence, they don’t grant any wishes true , knowledge with a second side gig is more fulfilling than putting money managed by these creative cons that are channeling financial risk investments , you are not promised any projected future controls, enough

Crashes happen, thats why your retirement and life shouldn’t have just one basket. 401k, IRA, Mutual funds, Emergency Savings, paying off debt… Guess what, the market gets back and grows more. You just have to wait. The poor people sell bc they are afraid and the rich hold on and make money.

This was a solid analysis of a dated 60 minutes segment which I have seen many times before. Just a few of my thoughts,.1)as a recent retiree I haven't lost 1 second of sleep during the recent market drop because I planned for downturns.2)one should never be as desperate and pitiful as those people who lost their jobs in 2008.3)always have a solid 3 or 4 years of cash reserves at all times to weather all storms.4)there is no excuse for people to not be educated about their investments now because of all the available information online.5)pensions arent coming back,..either are 8 tracks or VHS tapes.6)always live well below your means7)don't ever feel particularly rich when the market is up,…because it will go down.8)if you have a weak stomach for risk put your money in a cd or money market and earn nothing.9)there is a reason you hear the phrase ''past performance does not guarantee future results.10)the stock market owes you nothing.

Get the government hand out over everything

I think this illustrates just how painful an severe the 2008 crash really was. But lets not forget that there were some very unique circumstances occurring then. The 60 Minutes pieces was done at the very bottom. The market did recover and no it didn't take 10 years. If you had stayed with it, you did fine. If you threw in the towel, then you lost big. There are no ways to have a safe return. If you don't take on enough risk even in retirement, then you risk burning through your assets before you die. People make emotional decisions and rehashing this is just playing to those emotions. I do agree that financial education is a weak point in our society. But if you think about it, our society and economy are really built on the assumption of that ignorance. Somehow we all seem to get richer when we all endlessly consume.

I watched the movie The Big Short 4 times over a 4 yr period . People still trust n invest in the rigged stock market n it's pushers . Stupid in stupid out.People are losing their life earnings thru crypto also .Only invest the amount of money you can afford to lose .

What do you think in our current economy is comparable to cause a similar economic collapse to 2008? Further more, the original video is at best fear mongering. Do we need more financial literacy? Sure. But this isn’t the way to do it

The market always comes back, usually it comes back very quickly, dollar cost average into the market, 401k is a great thing ….this guy is not being honest in my opinion

I don't understand why the 60-minutes episode (or you?) didn't emphasize that the money would, based on history, recover in a handful of years. And indeed it did. Likewise all the money being lost on paper now will be recovered over time. In the good times people need to build up a reservoir of cash assets to carry them over during the downturns. Thanks for the episode.

"There but for the grace of god go I" and that can be said not just for me, but for most all 401K participants. Somewhere early in this video you call the 401K a "tool". Well I am a recently retired engineer (last year), so I will acknowledge it's a tool, but as was pointed out around 17:50 or so it was never designed to do the job its now supposedly doing. That dirty little secret is rarely if ever mentioned now days. Designing tools to be used in dangerous situations is something I have done in my career. Taking care to ensure the user of that tool can do the job they need to do safely, and has the proper training is always of paramount importance! In some situations the government (OSHA and other such agencies) plays an active role to make sure the tool is safe to use. How is it that we allow the "financial services" industry to put an ill-designed tool in the hands of common people, offer no training, and tell them their future depends on the proper use of it? I'm old enough to remember when 401K's first started coming out. The company I worked for back then was at that time a Fortune 500 company, not your average Mom & Pop grocery store. They had a decent pension plan and told us employees we would be taken care of. To that end they offered the "Savings & Investment Plan" as they called it as a way to supplement that pension. Fast forward 15 or so years, and a lot of bad decisions by the companies senior management, and suddenly there is talk of "sun-setting" the pension and now that 401K which hadn't changed a bit, was the retirement plan. By the time I left that company there were a host of "Mutual Funds" offered in that plan which consistently lost money. I still have a couple of those prospectuses. Why would anyone put their money in a fund that loses 2 – 8% every single year? Mostly because they became the only choices available. The company I retired from last year, also a Fortune 500 company, offers nothing but a 401K retirement plan to new employees. Why? Simple – It's the cheap and easy way out for the company. Management would pull no punches on that point. Every dollar not spent on administering a pension plan could go directly to BIG management bonuses, and though the language would be flowery and full of big fancy sounding words if you watched what went on in the company and thought about it for a minute or two the message came through. Asking too many questions could very definitely be a career threatening move! So why is this happening again? Well the fact the stock market is cyclical is one of the few things we were told about it when I was in school. From my vantage point after watching this play out over my 46 year career it all comes down to pure greed! Greed in the financial industry, greed in the elected officials who turn a blind eye to whats happening because they are paid off by lobbyist like the one in this video…

IMO you need 4 years of cash in addition to diversified growth stock accounts. 4 years so the market can repair. before one can even consider retirement and still there is no guarantee. My grandparents were very wealthy with businesses factories several houses and a large estate. In a nano second because of the wars in Europe it was all gone. Unfortunately for them my grandmother was also going blind from glaucoma so she could no longer work. I talked with someone from Cuba 2 weeks ago and the same thing happened to them. This is not uncommon. We can only hope the 2 oceans will still protect the US from all the crazy actors in the world. all one can do is put the odds in our favor and hope for the best. What happens happens. Everyone try to take care of their health..my sister died young from cancer. My brother and I both got cancer and so far have surv8ved. However, I have worked myself to death 60hr/wk for55 years and still do. My 95 y.o father has dementia. My other sister was hit by a drunk 40 years ago his 3rd DUI and suffered massive brain damage He was fined 10K and walked out of court and I have supported my sister ever since. And my grandfathers both dropped dead of heart attacks while at work at ages 55 and 58. Sometime I wonders what it is all worth but I just trudge on. Monday will be another busy work day with my only likely future fate is a heart attack like my grand parents, recurrence of my cancer like my sister or dementia like my father or another frivilous law suit. So all I can say is I do not give a rats behind or a nice way like Bobby MacFarin dont worry be happy.

I am 57years old

Hello I don't want to retire

this is old

this reality is sad…